Construction Loan Programs

Whether you're building from the ground up or improving what's already there, we're here to guide you through flexible loan options that fit your unique project and timeline.

Construction-to-Permanent Loan

Finance your entire build — from lot purchase to move-in — with one streamlined loan that automatically converts to a traditional mortgage once construction is complete.

Renovation

If you're planning to remodel, add on, or make major improvements to your current home or a fixer-upper, we offer renovation loans designed to help bring your vision to life.

Explore Renovation Loans ProgramConstruction Loan Features

Save time and money

Financing the lot and the construction in one loan that modifies to permanent financing automatically when the home is completed saves you time and money. It’s one simple process and one set of closing costs.

Locked interest rate and terms upfront provide peace of mind

With the interest rate locked at closing, you know exactly what your principal and interest payment will be when the home is completed. We offer construction terms of 12 months, and you can customize your timeline after consulting with your builder.

Lower interest-only payments during the construction phase

With a Construction-to-Permanent Loan, you’re only charged interest on the money advanced toward your project, making the construction phase more affordable. As your builder completes phases, both the interest due and the amount advanced increase.

Simple draw process including a dedicated Northpointe team to assist

Your builder will request draws from your construction loan to pay for work completed on your project. Northpointe’s dedicated construction team manages requests, inspections, and title validations promptly to help keep your project on schedule.

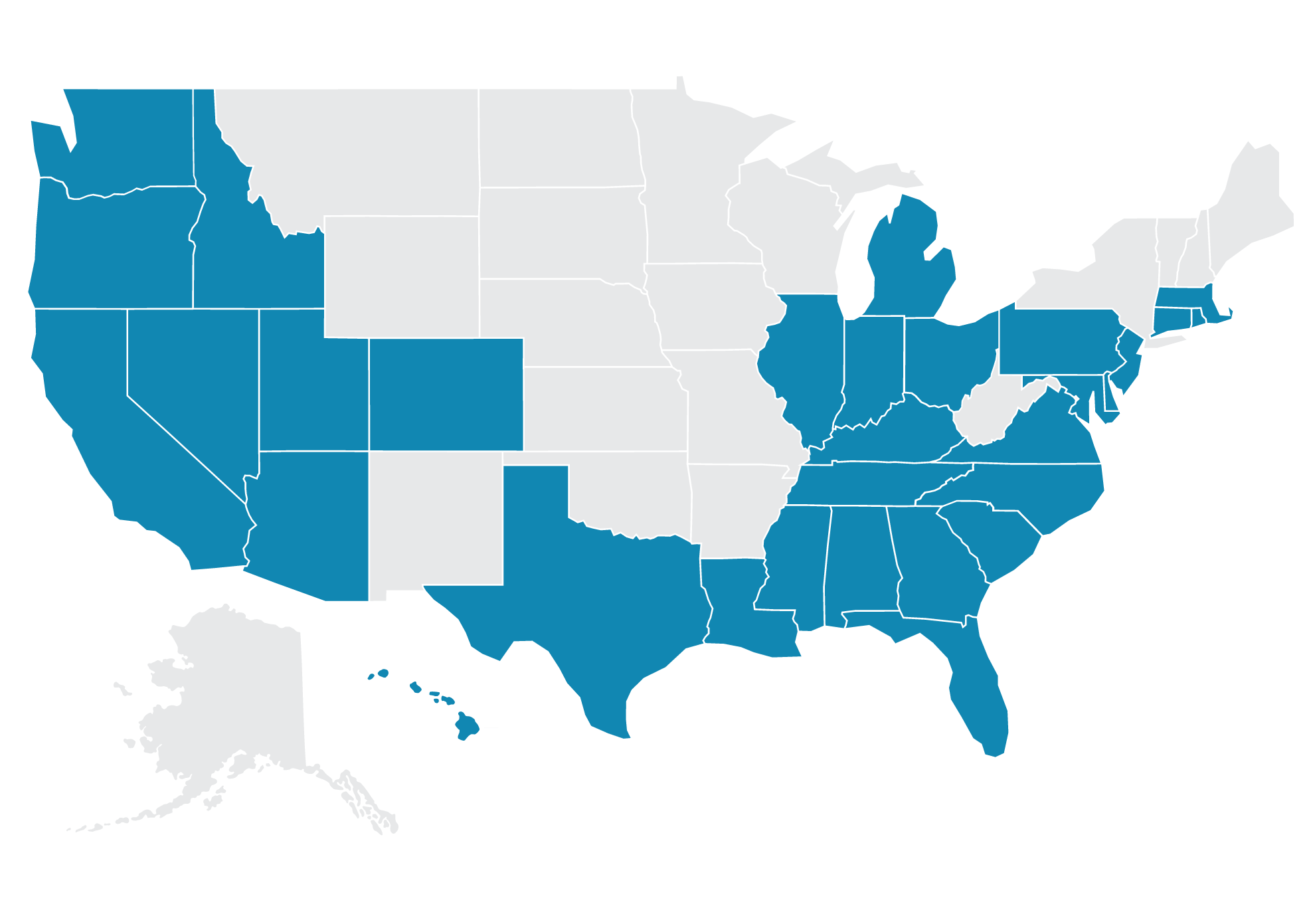

Where We Lend: Construction Loans Available in 31 States*

Northpointe Bank proudly supports homebuyers and builders across 31 states with flexible construction lending solutions. Whether you're breaking ground on your first home or tackling a major renovation, we’re here to help make it happen.

Got Questions? We’ve Got Answers.

Explore answers to common questions about our construction loan process, financing options, and what to expect along the way.

When should I choose a builder?

Selecting a builder to work with is among the first decisions in building a custom home. It's essential to choose one based on client references, online reviews, and the ability to deliver on time and within the agreed-upon budget. The right builder will provide you with the construction and home plan information necessary to put your project together. They can also perform a site survey to confirm the ability to build your home plan on a selected site.

When should my pre-approval be in place?

Pre-approval is a crucial early step; it allows you to know what you can borrow, along with providing a budget. These budgets help understand the relationship between the costs and how much to allocate to different aspects, such as land, pre-construction site development, and the home itself.

Can I acquire land with my construction loan?

Land can be acquired with a purchase agreement through the construction loan process. After your project plans and budget are finalized, you can close on your loan, with the first draw amount paid to the seller of the land. It is recommended to allow 90 days to close after the mutual acceptance date.

How does a contingency work?

A construction contingency is an amount of money set aside to cover any unexpected costs that can arise throughout a construction project. This money is on reserve and is not allocated to any specific area of work. Essentially, the contingency acts as insurance against other unforeseen costs. Any leftover contingency amount will be applied to the loan balance when the home is completed.

Can I lock my rate?

You can lock an interest rate prior to closing your construction loan early in the process, providing peace of mind. Your interest rate will remain the same during the construction phase and when the home is complete for the life of the loan.

When does my loan fund?

The construction loan funds when the documents are signed at closing. An amount may be advanced at closing to purchase the lot if applicable and provide reimbursement to your builder for permitting, plans, and other costs already incurred. Interest payments will be due on the first of the following month.

What happens with my loan once the build project is complete?

Northpointe Bank will modify your construction loan into a permanent home loan; there's no need to refinance. We perform an examination confirming the final loan amount based on what is actually drawn. Once the modification is complete you'll start making your principal and interest payments.

Can I get a loan for just land and build later?

Yes, Northpointe offers loans to acquire land. You can refinance it into a construction loan when you are ready to build. There are no prepayment penalties on land loans, so you can reduce the principal or pay it off any time.

Read more on our blog

Ready to learn more about Construction loans?

Connect with Construction Lending Manager, Andrea Stadler.

This is not a commitment to lend. All loans are subject to credit review and approval. Other terms and conditions may apply.